Bretton Woods out with a Bang!

This is not 1944, 1971 or 2008, it is all three.

Good Morning - The Global-Dollar-System (GDS) and the Bretton Woods framework that birthed it is unwinding. That was the conclusion of the Li Ruogu, Chairman of the Export-Import Bank of China in 2009. Li told the Financial Times:

“The financial crisis caused the global economy to suffer heavy losses, and it also let us clearly see how unreasonable the current international monetary system is. But it would be difficult to find and implement a feasible replacement plan in the short term, so we will still have to travel a relatively long road for reform of the international monetary system”

Li Ruogu

A decade and a half later the dollar has finally arrived at the end-of-cycle destination charted in 2008. Utterly missing the forest for the trees, Donald Trump and his lobotomized Cantillionaires (Howard Lutnick, Scott Bessent, Peter Navaro) are attempting to reindustrialize the US economy while preserving the dollar’s status as the world reserve currency. They are discovering that achieving both simultaneously is impossible, and second, that weaponizing one (the dollar) via sanctions, confiscations, or chaotic tariffs to rebuild the other (US industry) will destroy both.

Weaponizing the dollar via sanctions, confiscations, or chaotic tariffs to rebuild US industry will destroy both.

The United States is a nation desperate for revolutionary reform, not conservative tinkering exaggerated by media bluster. Unfortunately, the Trump Administration lacks the historical perspective, strategic vision, or the executive agility to adjust to the post-Bretton Woods world. In practice, Trump is trying to salvage a monetary order hatched at the end of World War II, warped in 1971, and irreparably mangled in 2008. Rather, Trump’s triumvirate are revanchists who believe America has all the leverage:

The world cannot function without New York City stocks, banks and bonds

US consumers fuel global trade

Dollars are the unassailable standard for global transactions.

These assumptions no longer define a transformed 21st century monetary order.

The Trump train is sailing listlessly into the end of cycle storm full speed ahead. Today, we are faced with the convergence of inescapable long-term trends punctuated by short-term emergencies. Long-term monetary cycles indicate the dollar’s run as world reserve currency is expiring, and a hundred year top approaches in the US stock market. As unnerving as these warning signs are, the explosion of government deficits, stunted global growth, and Sino-American rancor augur a financial finale for the GDS.

Will trade war with China finally trigger the dollar’s demise or is Trump’s tariff flex priming the world for a new grand bargain, a post-Bretton Wood’s monetary world order? Let’s find out.

Twins Deficits and Dilemmas

Twin deficits (trade and fiscal) bedevil America’s economy. Both have systematically emaciated the middle class and unraveled its once world-renowned industrial prowess. Fiscal deficits are choking off or “crowding out” much needed capital investment for the private sector to fund unproductive, exorbitant entitlement programs and military-industrial-grift. Meanwhile, trade deficits have dwindled the manufacturing base while financialization has ripped apart what’s left of America’s middle class and small business economy. Unfortunately, twin deficits are endogenous to the GDS; it is a feature not a bug.

Twin deficits are endogenous to the Global Dollar System.

In the long run, reserve currencies prove to be poison pills. Robert Triffin identified the conundrum in the 1960’s when he noted that reserve currency nations were required to export more currency than goods to provide excess reserves to foreign powers who need them to transact. Initially, the trade off makes sense because the network effect spreads the currency, making it central to global trade, investment and banking, and guarantees the reserve nation has a permanent line of credit since they can borrow in their own unit of account while everyone else cannot. Overtime however, the financial system of the host country grows like a cancer, slowly eating away at productive industry or real economy - a process called deindustrialization.

Financialization exacerbated the imbalance inherent in Triffin’s Dilemma. While some degree of trade imbalance was inevitable as dollarization spread far and wide, Wall Street and Fortune 500 elites eagerly dismantled America’s industrial suite to maximize shareholder value, leaving entire regions of the country from the Rust Belt to Appalachia stripped bare and hollowed out. As factories, supply chains, and feeder systems closed up shop and migrated overseas, industrial communities from Detroit and Cleveland to Chicago and Philadelphia disintegrated.

More importantly, America lost her industrial-economic dynamism. What Robert Gordon calls General Purpose Technology (GPT) is the multiplier effect of productivity. If you have the factory floor you are more likely to have the adjacent industry, expertise, and tangential “subinventions” that feed on the original invention. For example, after World War II America refit entirely its wartime industry to build a peacetime economy. Gordon summarized the transformation like this:

“In 1946-1947, the floodgates of demand were let loose, and after a swift reconversion, manufacturers strained to meet the demand for refrigerators, stoves, washing machines, dryers, dishwashers, not to mention automobiles and television sets…Every part of the postwar manufacturing sector had been deeply involved in making military equipment or its components, and the lessons learned from the war translated into permanent efficiency gains after the war.” Robert Gordon - Rise and Fall of American Growth

Put more succinctly by Gordon, “technological change does not regress” provided you maintain the industrial apparatus, human capital and infrastructure required to sustain it. However, without industrial scaffolding you don’t simply lose factory jobs, you lose the entire ecosystem of innovation, and rebuilding one becomes extremely difficult.

Tariffs to Trumptopia?

Unfortunately, neither Wall Street elites nor Techbros in Silicon Valley fully comprehend the malignancy of financialization because they are a part of it. Wall Streets schemes are infamous but Silicon Valley has degenerated into an entrepreneurial grift “transforming entrepreneurship from a productive activity into a consumable, mass-marketable good fit for conspicuous consumption.” As a result new companies are a declining share of the economy, few experience scalable growth, and this appears to be “systematic.” Instead, President Trump has crafted an alternative narrative in which America’s decline is solely the result of poor trade agreements, exploitative foreigners, and inept Washington leadership. While Trump is right about DC’s fecklessness and poor trade deals (NAFTA for example), the balance of trade problem is a symptom not a cause of the cancerous GDS.

“In this sense, the Entrepreneurship Industry is perhaps best thought of as a ‘Muppet Factory’: an industrial-scale manufacturer of products and services ultimately produce poorly performing ventures.”

Towards an Untrepreneurial Economy? - Rasmus Koss Hartmann et al

Blanket tariffs on the world are a reflection of bankrupt thinking. First, since financialization and deindustrialization are features of the GDS, solutions to America’s decline require internal reform first, what I refer to as definancialization. Second, reindustrialization is not the same thing as reshoring, and neither problem is something tariffs can solve. Finally, the immediacy of America’s financial problems suggest we need to fix fiscal deficits before we address trade deficits. Basically, the President’s team is confused about the order of operations needed to address America’s economic moment or perhaps they are unwilling to admit the scale of the problem.

Definancialization is the precondition for America’s economic salvation. Financialization, or making money through a complex web of financial transactions rather than creating real goods and services people actually need, defines the practice and philosophy of America’s techno-corporate elite. Under their leadership, America has become a financial system with an economy rather than an economy with a financial system. Companies do not invest in plant and equipment, training and hiring new staff, or focus on the long-term strategy to secure the company’s future. Rather, corporate boards mothball capital investment because it is too expensive, downsize staff to skeleton crews to reduce overhead, and buy back stock to prop up market valuations. Corporate bonuses, mergers and acquisitions, and selling preferred stock during IPOs dominate their focus, safeguarding the future of the companies they run is not a priority.

A February 2021 activist letter diagnosed the failure of America’s techno-corporate elite better than I can:

“In 2010, Kohl’s top five executives earned a healthy $20 million in total compensation, at a time when sales were $18.4 billion and operating income was $2.1 billion. Fast-forward to 2019, when sales had increased slightly, to just under $19 billion, but operating income had declined by ~42%, to $1.2 billion. While one may think that such weak results should justify lower executive pay, compensation for the top five executives instead increased to $30 million in 2019.

This is made possible by an arrangement, approved by the Board, that pays executives a target bonus for achieving declining sales results.”

While affecting a shift in techno-corporate culture is a high bar, the US government could begin the process by implementing structural reforms to entitlements to balance its budget. Doing so could free up trillions needed to reliquify industrial capitalism. Short-term, there would be adverse effects (a recession or worse) and aggressive backlash from a population drunk on government dependency. Indeed, the withdrawal period is a painful but necessary step toward sustainable convalescence. Even said, reindustrialization is a national project that requires a root-and-branch rebuild of American infrastructure, industry and a reorganization of the US government.

Unsafe “Safe” Havens

By foolishly reversing the order of what needs to be fixed first, Trump’s tariffs have proved that treasuries and dollars are no longer safe havens. Mere days of disruption post “Liberation Day” forced the Fed to bailout hedge funds playing the Basis Trade and wiped out trillions in market capitalization on Wall Street. More importantly, the value of the dollar relative to other currencies (DXY) fell and treasuries collapsed in value. These developments were completely unanticipated by Trump’s team and the Cantillionaire class who dogmatically believe that America’s monetary dominance is unassailable. That is simply no longer the case, and it has not been for some time.

The problem is simple, America’s financialized-economy depends upon foreign investors parking profits and investments in USD denominated assets (banks, bonds, stocks, real-estate) but foreigners do not depend on US consumers, resources, or industry. Specifically, when it comes to China, America depends on Chinese manufactured goods but China does not depend on US exports or consumers. As Jeff Curie explained in a recent interview, China’s manufactured goods are non-fungible, meaning they cannot be easily replaced, whereas America’s exports, primarily oil, natural gas and agro-commodities are fungible, they are replaceable.

Decades of persistent and indiscriminate sanctions, confiscations, regime changes, and vulture capitalism against the non-Western world has forced the Global South to reorganize over the last twenty years. New trade groupings like ASEAN, BRICS and SCO, new supply chains in Eurasia, Asia, and South America, and the consolidation of natural resources in BRICS+ has fundamentally remade the global economy. Western hypocrisy in Gaza, proxy war with Russia, bellicosity toward Iran and now trade war with China has finally broken trust in the US as a reliable business partner or safe haven. So they are slowly divesting tens of trillions in assets from US markets.

Trust in the US as a reliable business partner or safe haven has finally broken.

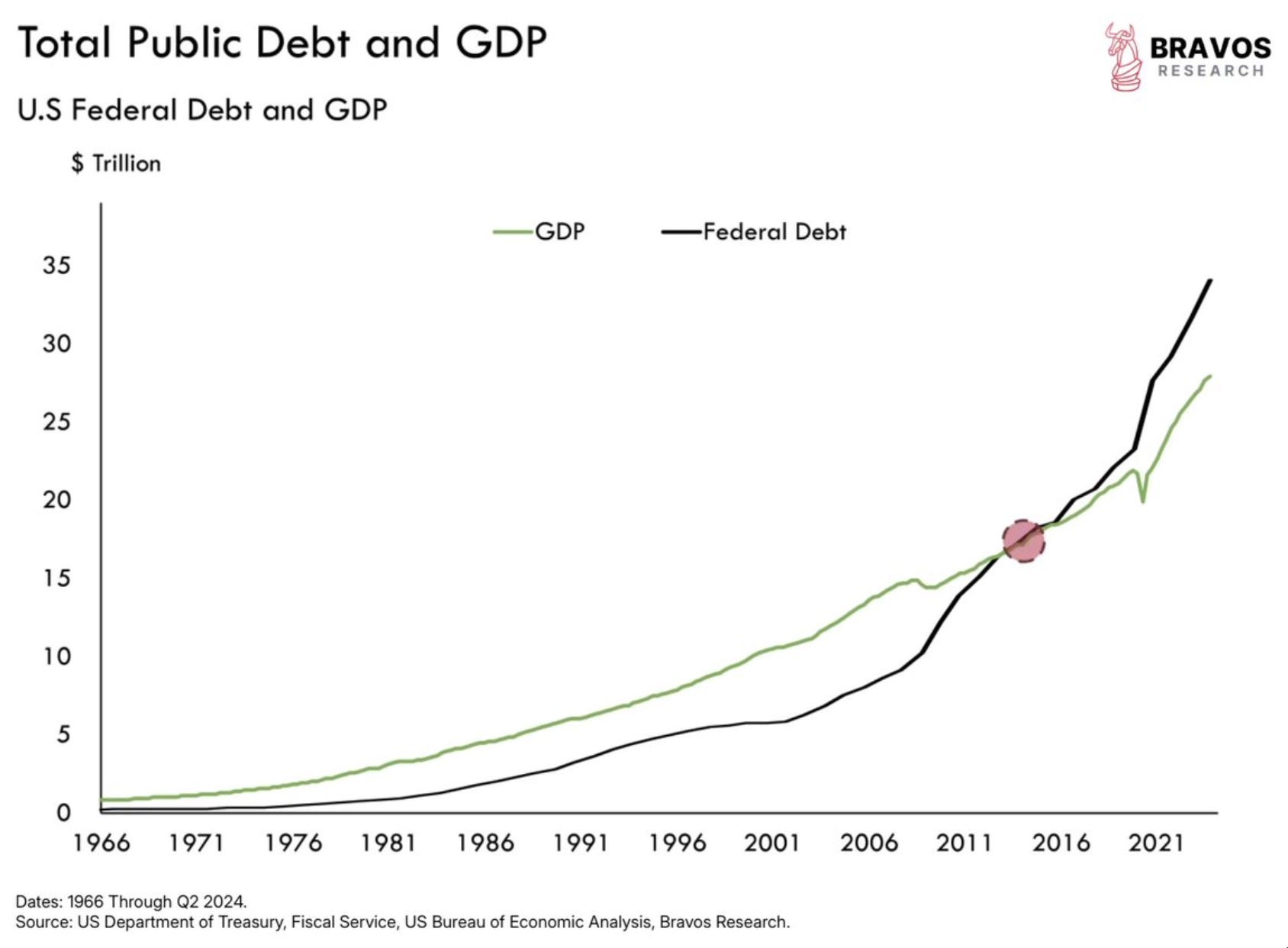

If America’s monetary missteps overseas are not bad enough, its brittle internals paint an even bleaker picture. The Treasury must refinance $10T in debt over the next two years and there are not enough buyers to do so. Yields are beginning to move non-linearly (see below), independent of monetary authorities or government officials and will continue to rise because inflation remains high and the economy is slowing. Most importantly, because the US government (USG) is on the hook for at least $175T in unfunded liabilities incurred through entitlement programs, military pensions, and countless other programs its room to maneuver is gone. The USG is structurally insolvent.

The US economy is equally imperiled. Inflation remains high, unemployment is much higher than widely reported, industrial production is anemic, and a trade war will exacerbate these trends. Chinese tariffs on US goods will hurt farmers and sinking oil prices will crush US shale production while raising prices on everyday items. Add to this DeepSeek AI’s open source breakthrough in January, which destroyed Silicon Valley’s semiconductor value proposition and popped the AI mania along with it. A peak under the hood in the housing market, commercial real-estate, or shadow banking derivatives like CLOs reveals a hyper-financialized economy on the brink of a sudden and severe contraction.

End of an Era

On the eve of war in July of 1914 the global financial system spiraled into hysteria. Despite the assassination of Archduke Ferdinand in June, global markets did not panic until Austria’s ultimatum to Serbia in July. Overnight, animal spirits screamed into a full panic and the race to raise capital was on: bank runs, stock crashes, and money markets ruptured as investors rushed to withdraw money, prompting the London Stock Exchange to close for the first time in its history. Long queues for gold coins began in London, panicking confused onlookers who thought they were watching a run on the banks. The Bank of England (BOE) responded swiftly by suspending the Bank Act, allowing them to issue Treasury notes and institute long bank holidays.

The end of Pound Sterling as reserve currency seemed imminent but it wasn’t. A full month into the crisis pressure from London banks to suspend the gold standard was feverish but a young advisor to the Treasury convinced David Lloyd George, the Chancellor of the Exchequer, not to suspend the gold standard. The precocious John Maynard Keynes reasoned that since Great Britain was the world’s creditor and safe haven so eventually gold would flow back to London, and that is what happened. While Chancellor George employed massive monetary intervention and created the template for Fed operations a century later, he never suspended the peg to gold and Pound-Sterling survived as the reserve asset.

While BOE gambits staved off a total meltdown in 1914 by the 1920’s a shift in monetary power was well underway. Great Britain’s losses in WWI notwithstanding, American economy had also overtaken a British Empire in decline. Studies of foreign exchange holdings reveal that post-WWI investors began to pivot away from London in favor of New York City, and increasingly held dollars as much as pounds. The Bretton Woods Agreement - ironically architected by John Maynard Keynes - made the monetary shift official in 1944, but it could be argued there were dual reserve assets by 1930.

A shift in the monetary order of perhaps even greater proportions has been underway since 2008, and the blowback from Trump’s tariffs have confirmed it. The Global Financial Crisis marked the beginning of a shift in economic power towards Asia, the establishment of the Shanghai Gold Exchange International (SGEI) in 2014, and buried Western governments and economies in insurmountable debt and sclerotic growth. By 2020, Covid lockdowns, supply chain disruptions, and the deluge of stimulus that followed spiked inflation, severed global trade, and unanchored interest rates. When the Fed and CBs responded with historically aggressive rate hikes the debt bomb was finally triggered.

Global Collapse or Grand Bargain?

Signs of reordering into a Multipolar Monetary World Order (MMWO) have only multiplied since 2020. The dollar’s diminution is manifest across domains: geopolitics, gold, and monetary realignment. The failure of Western sanctions against Russia was a proof-of-concept that shocked the West and inspired the East. BRICS members and beyond learned that procuring natural resources and gold, selling Treasuries, and constructing alternative payment rails and trade unions are the guarantors of their protection. Likewise, Chinese bankers and Middle Eastern oil sheiks have pivoted accordingly, and swing states like Saudi Arabia, Turkey and India are leaning into the MMWO by ignoring Western sanctions against Russia, embracing BRICS and opposing Israel’s wars.

The non-Western world has reached a consensus that dedollarization is essential to resist the weaponized dollar.

The non-Western world has reached a consensus that the GDS is no longer viable. Victor Gao - Chairman of the Center for China Globalization (CCG) - summarized the Global South’s position well when he said “I personally am not a fan of dedollarization, but I really firmly oppose weaponizing the dollar.” Unfortunately, Trump’s Cowboy Diplomacy has rendered dedollarization essential to resist the weaponized dollar. In a speech to industrialists this month Putin confirmed that a monetary schism was not a temporary condition but a permanent fixture of the MMWO:

“Sanctions are neither temporary nor targeted measures; they constitute a mechanism of systemic, strategic pressure against our nation. Regardless of global developments or shifts in the international order, our competitors will perpetually seek to constrain Russia and diminish its economic and technological capacities.”

President Putin

Under such trying circumstances a grand bargain is virtually impossible because the source of America’s plight is in DC, NYC, and Jerusalem, not Beijing, Moscow, or Tehran. America’s relationship with the rest of the world vis-à-vis dollar diplomacy (or any form of diplomacy) has been permanently damaged. Until there is fundamental change in the governance of the West, until control of the USG and economy is wrested from Zionism, Wall Street, and Silicon Valley, America is condemned to secular economic decline, demographic destruction, and perpetual war. The spectacular failure of MAGA less than 90 days into Trump’s ill-fated second term proves that only a market accident, national crisis, or lost war can reset America’s leadership.

The spectacular failure of MAGA proves that only a market accident, national crisis, or lost war can reset America’s leadership.

The real story however, is that the US is entering a deep depression, which is unleashing a financial, economic and social-political nightmare all at once. As difficult as the unwind will be it is a prerequisite for America’s resurgence. Indeed, the Trump administration will be the sacrificial lamb to definancialization. Doing damage control this past week, what Scott Bessent dismissively called “deleveraging convulsions” is the clarion call. Markets sold off because of underlying economic weakness and financial fragility, sinking dollars and Treasuries simultaneously. At the center of the turmoil is the breakdown of the GDS and the end of Bretton Woods, the true source of America’s misfortune.

Welcome to the end of cycle.

Stay liquid, stay alert.

I completely agree with the historical parallels — in fact, I reached many of the same conclusions long before reading this article. But my interpretation diverges in several key areas.

First, Trump’s actions aren’t “chaotic” or “lobotomized.” They’re non-consensus. He’s not playing the polite, technocratic game — he’s tearing up a rulebook written by the very elites who hollowed out the West. The article critiques tariffs, but what’s the alternative? More financial alchemy, more central bank doublespeak, more slow decay dressed up as progress? Trump isn’t papering over the symptoms — he’s ripping out the rot at the root.

He’s targeting the CCP where it stings — their offshore wealth, their backdoor deals, their hidden influence. He’s driving wedges into elite alliances and forcing countries to make a choice: align with the U.S. and enjoy zero tariffs, or get bypassed entirely. It’s that simple. And let’s be real — debt means nothing if you can’t enforce it. Power enforces contracts. And the U.S. still has that leverage.

Everyone loves to say “China,” but no one says Chinese Communist Party. It’s not about the people — it’s about the regime. People like Rachel Reeves would rather cozy up to authoritarian technocrats than cooperate with Trump. But he’s the one exposing the Crown Corporate oligarchy still ruling over Europe, the UK, and their offshore empire.

Remember when Trump slapped tariffs on “Penguin Island”? The media mocked him — but he was exposing the Crown’s shell structures and tax avoidance networks. That wasn’t ignorance. That was precision. And the press, in their knee-jerk reaction, revealed just how deep they’re entangled in that very system.

The article warns of “American overreach,” yet says nothing of China’s fragility. The CCP cannot afford a Trump success. Their military is second-rate. Their real job is suppressing their own citizens. A Taiwan blockade? That’s not power — it’s suicide. Trump would happily absorb Taiwan’s industry and know-how into the U.S., collapsing China’s export leverage in one move.

A reindustrialized U.S. doesn’t just shift global supply chains — it ends the CCP’s economic model. That’s why they’re scrambling for gold, building bilateral trade routes, and trying to carve out a new role in a monetary order they no longer control. Not from a position of strength — but fear. Fear that the real economy — not fiat — will define the next global standard.

Trump isn’t deluded. He’s one of the only leaders responding to the world as it is, not as it used to be. Everyone else is still stuck in a 1971–2008 fantasy, hoping debt, diplomacy, and ESG slogans can delay collapse.

That’s not strategy. That’s denial.

And let’s kill this tired narrative once and for all — Trump dumb, China genius. No. China still depends on Israel for core military tech. The CCP doesn’t innovate — it imitates. You can’t claim to be a dominant power while outsourcing your breakthroughs. Same goes for Russia.

Meanwhile, Trump is beating Europe over the head with its own stick. Look at Germany: building Nord Stream while funding NATO. Paying billions to Russia while claiming to protect against them. Who runs that racket? European oligarchs — Trump exposed that. And now he’s pulling U.S. defense away from Europe. He called Zelensky a dictator — just days before the UK-Ukraine treaty was meant to be cemented. That voids it. He’s not playing along anymore.

Europe will print itself into oblivion. That’s why gold is going up. But the U.S. dollar won’t fail. The EU is crippled by debt, bloated social schemes, and a total absence of hard power. They offshored manufacturing to China — which, let’s not forget, is Russia’s ally. Trump’s message is simple: you align with the U.S., or you get left behind.

This isn’t about Trump the man. It’s about tearing down a parasitic oligarchy — one that exported your jobs, imported China’s surveillance tech, and now wants you to worship unelected central bankers flown in from Canada.

Trump is at war with the old Crown Corporate Empire. And he’s winning. That’s why they’re terrified — and why the fear campaign is always “China this, China that.”

But here’s the truth: the world shouldn’t fear China. It should fear the United States.

Under Trump, America is finally remembering how to use its power. They've tried to KILL HIM TWICE.

“Babylon hath been a golden cup in the hand of the Lord, that made all the earth drunk: the nations have drunk of her wine, and therefore they have staggered.”

-Jeremiah 51:7